Swedish industries are moving towards a recession.

Spoiler: Swedish industries are moving towards a recession. The Diffusion Index has declined since its peak it May 2021. Even though it is fluctuating above zero, it is declining indicating that production in an increasing number of industries is declining compared to twelve months earlier. The Diffusion Index shows the development until August 2022.

The developments for especially Service industries are negative reflecting pessimistic expectations of future income. Also, developments of individual manufacturing industries are declining. Production in the intermediate goods industries, especially its energy-intensive part, is declining. Production in the durable goods industries is also declining reflecting expectations of lower future incomes and higher interest rates.

A high inflation and declining production indicate that the economy might be heading towards stagflation. A tighter monetary policy which is needed to curb inflation will have adverse effects on employment and production.

This is an update of my previous post

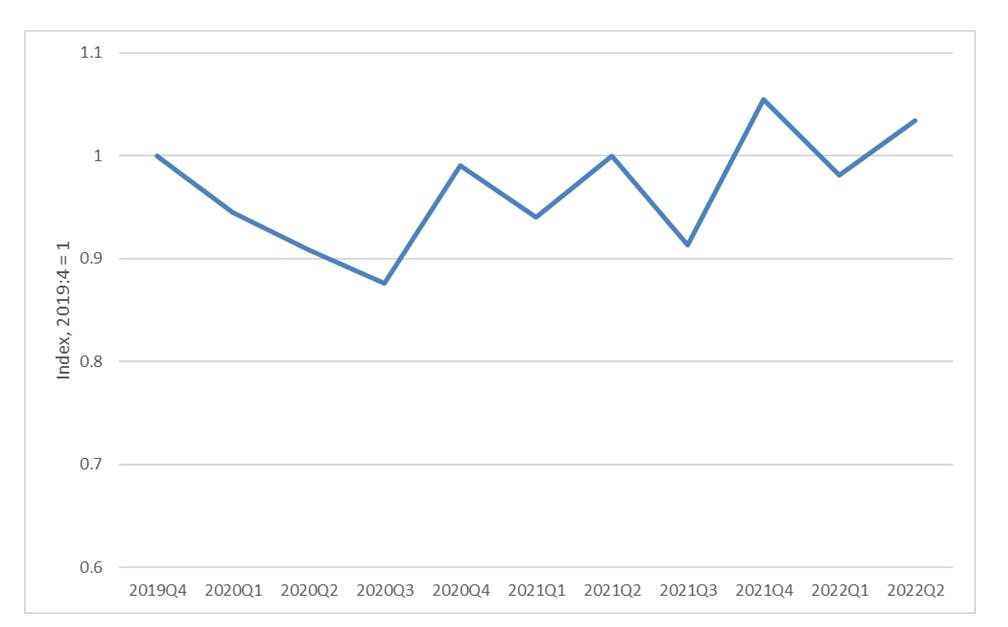

which itself was updating previous posts on the same subject. Since the last post, showing GDP until 2021:4 Swedish GDP has decreased slightly, c.f. Figure 1.

Figure 1. GDP in Sweden 2019:4-2022:2, index 2019:4 = 1.

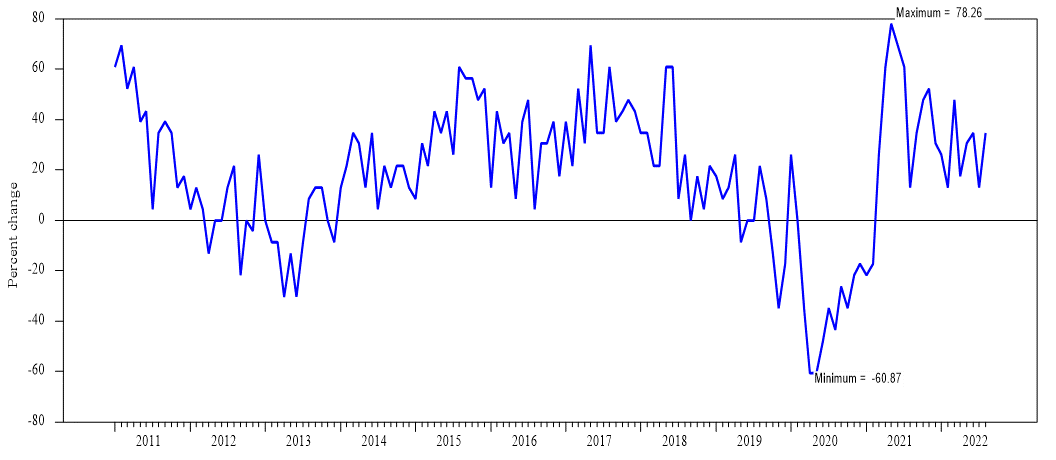

As in previous posts a Diffusion Index shows the overall situation for aggregates of individual industries. The index is calculated for forty-six different industries and shows the difference between the percentage of industries that are growing and the percentage of industries that are declining. Growing means that an industry’s production value index is increasing compared to 12 months earlier. Declining the opposite.

The graph below shows developments between January 2011 and August 2022. Following the outbreak of Covid-19, the diffusion index declines sharply and reaches minus sixty-one in April 2020. That low is then the benchmark for the high values a year later in April and May 2021. The maximum of seventy-eight was reached in May 2022. The following months witnessed a return to less extreme values. Though fluctuating above zero, the index is gradually declining, c.f. Figure 2.

Figure 2. Diffusion index for Swedish industries, 2011:1-2022:8.

Source: https://www.statistikdatabasen.scb.se/pxweb/sv/ssd/START__NV__NV0006__NV0006A/PVI2015FastM07/table/tableViewLayout1/ Note: Public services industries P-Q were only available until 2021:12. The development 2022:1-2022:8 was updated by the development of the aggregate total services. The transportation services industries H49-H53 developments 2022:7-2022:8 were updated using the whole aggregate H development for that period. Similarly, the aggregate business services J-M was used to update services industries J58-J63.

Data for all industries is only available to December 2021. The note below Figure 2 indicates the industries for which extrapolations were made. There is however data for 31 of the 46 industries until December 2021. Calculating the Index for these yields twenty-three indicating a decreasing activity.

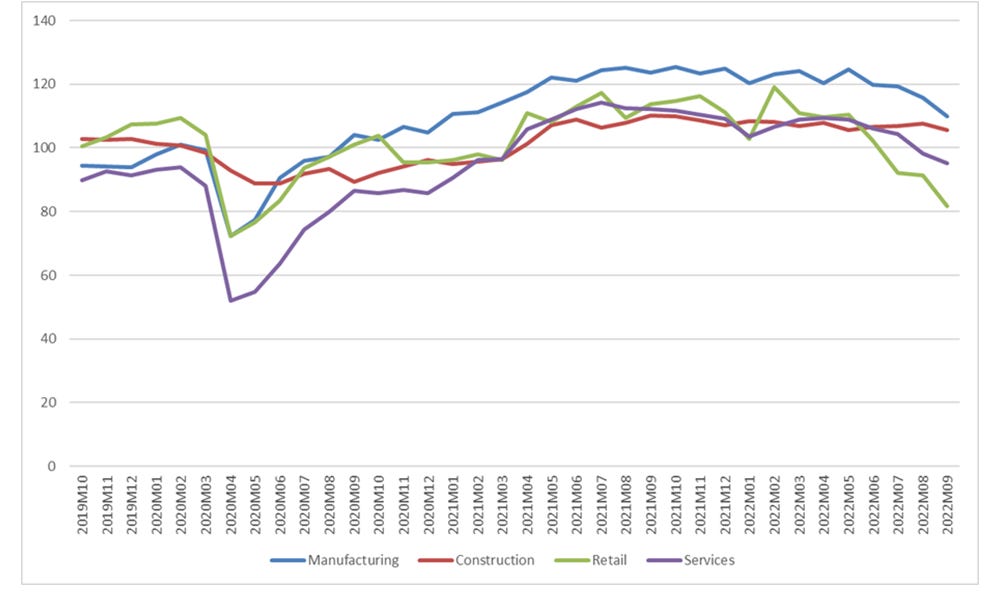

Looking at the developments of broader aggregates, the production of Non-durable goods industries is the only which continues to grow. Durable goods and Capital goods industries which are more sensitive to changes in income and interest are beginning to decline. That applies for the services industries aggregate Trade as well, c.f. Figure 3.

Figure 3. Production value indices for main industrial groupings and trade, 2021:1-2022:8, index 2021:1 = 1.0.

The production value for Total services is still increasing but that may change soon according to the latest Purchasing Managers’ Index for the Swedish services industries. While still above 50 in the month of September, the quarterly version of the index, for the third quarter showed a declined by eight units compared to the second quarter. The Industry PMI declined for the fourth month in a row and is now lower than 50 which means that more than half of the respondents report declining activities.

Developments in especially Retail Trade are alarming. Bankruptcies increased by 45% in September compared to 12 months earlier. This development is confirmed by the Swedish National Institute’s Economic Tendency indicator which looks beyond August. The indicator fell 6.4 points in September to 90.8. The Consumer Confidence Indicator hit a record low at 49.7. “All questions included in the indicator contributed to the decline, in particular how consumers view the outlook for their personal finances over the coming year.” It is therefore not surprising that the confidence indicator for retail trade declined to 81.7 and that bankruptcies in this industry are increasing.

Also, the confidence indicator for total Services is lower than normal while the confidence indicators for Manufacturing and Construction + Engineering still are above normal although weakening compared to previous periods, c.f. Figure 4.

Figure 4. The Swedish Economic Tendency Indicator for main aggregates of industries.

Source: The Swedish National Institute of Economic Research, https://www.konj.se/publikationer/konjunkturbarometern/konjunkturbarometern/2022-09-28-hushallen-an-mer-pessimistiska-och-naringslivet-backar.html Note: The indicators are standardised with a mean of 100.

After several months with increasing employment, August data show a slight decrease. Employment is however still very high and the only indicator in the Statistics Sweden’s Business Cycle Clock which is indicating an expansion. Most of the indicators point towards a declining economic activity.

Increasing inflation and decreasing production at the same time sounds like we are heading towards stagflation which is defined be negative supply and demand movements. We are not there yet and hopefully we can avoid it. Sweden has a flexible exchange rate. Monetary policy is more effective than fiscal policy in this circumstance. But the objective of the monetary policy is to curb inflation. And a tighter monetary policy reduces production and employment.